Hands down, one of the best decisions I’ve made in my financial journey is committing to a hybrid (digital and paper) budgeting system. It’s taken me to new heights financially that I honestly didn’t think would be possible until we were back to receiving two incomes.

In this post, I’m going to outline all of the reasons I swear by this two-part approach as well as my personal success stories. By the end, I’m confident you’ll be convinced and will want to adopt a hybrid system for yourself, too!

Now I know what you’re thinking…”Rach, it’s hard enough to maintain ONE budget…you want me to manage TWO?! Hard pass. It’s a no for me, dawg. Next!“

But I encourage you to read on with an open mind! This system is much easier than you think.

Before I start listing all of the reasons why hybrid is glorious, let me explain how I reached this point in the first place.

I’ve been budgeting in an Excel workbook since 2013. The first few years, my spreadsheets were a HOT MESS. I listed income and I listed expenses but there was no true vision. There were no goals. I was still making dumb financial decisions despite the fact I had a budget.

It just goes to show that the WAY in which you budget matters tremendously, and understanding your motivation for financial freedom is crucial.

It wasn’t enough to simply have a spreadsheet, because I couldn’t see myself in it.

I can’t emphasize that last line enough. You wanna know the secret behind getting out of debt early?

The golden ticket to financial freedom?

It’s not cutting out Starbucks. It’s not going a whole year without travel and only having date nights in. (These things could be part of the solution, but they’re not the spark.)

The secret is this: you find your motivation and you plant it in every single direction. You make your financial plan less about numbers and more about YOU. You pour yourself into your budget and you make it matter.

Go ahead and ask yourself now, “Why did I click this blog post? Why am I reading this?”

The answer is likely that you want help. Why? Do you want to stop living paycheck to paycheck and free up funds to see the world? Are you ready to finally start that business but you don’t have the capital? Do you simply want to set a positive example for your little ones?

Dig deep and define your WHY.

When I did this very exercise in 2016, I realized my why was my husband and future children. I fixed my eyes ahead and I never looked back. It sounds corny, but this is when my budget came alive!

I continued to track everything in an Excel workbook only, all the way up until this past winter.

In that time, I applied the Money Mantra (before it had a name), crushed nearly $100,000 of debt, funded a wedding, honeymoon, and 2-week vacation to Europe in cash, built my retirement funds to $20,000, and started saving to buy our first home.

You might look at the accomplishments and say, “Well, sounds like you did something right! If it ain’t broke, don’t fix it! (We love that saying where I’m from.)”

But here’s the thing.

We need to push harder. First, we are now down to one income and despite the numerous wins I listed above, we still have two car loans to crush before we’re completely debt free. Second, we formed some bad habits and let overspending go on in certain categories for far too long. And we don’t want to just “make it” during this time that I’m not working. We want to thrive!

Read: 2020 Life Update

That requires us to get our hands dirty and fine-tune.

So at the turn of the new year, I stepped into the unknown: the land of budget worksheets, cash envelopes, savings trackers, and all things ‘budget binder.’

BEST thing I could have done.

Okay, now that you know how I arrived here, allow me to elaborate on why I’ll never go back! Here are all the reasons to maintain both a digital AND a hard-copy version of your budget!

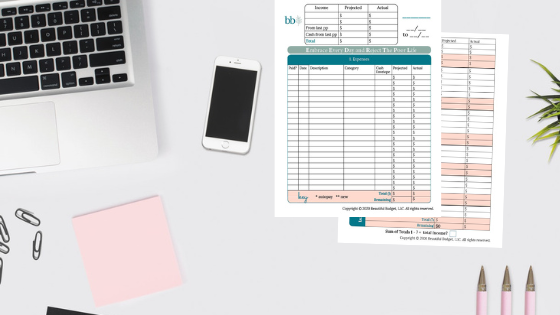

1. The Power of the Digital Draft

When you draft your budget digitally, you can make all the mistakes and changes you want. Copy, paste, delete, bold, new tab, new line, remove a line, change text color, add a category, rename a category – you see where I’m going here. Plus, you’re not limited on space. You can modify to your heart’s content until you get your budget just right! Once all of your projected income and the Mantra are filled out, all you have to do is transcribe the numbers and names onto your worksheets.

2. The Spreadsheet Includes Your Calculator!

Budgets can involve quite a bit of math as they become more involved, which opens up more room for errors if you only do them on paper. I don’t have to worry about this if I start and end my budget digitally. Excel performs the calculations for me (and even creates visuals like pie charts if I want it to.) I prepare my printed worksheets with confidence because I know the digital side was the heavy lift with all the calculations.

3. Copy Over Confirmation Numbers

All it took was one time in 2014 when a company “lost” my payment for me to make this a habit. (And no, I didn’t have a confirmation email to save me. They claimed a “glitch” occurred despite the payment clearing my checking account. Never again.) I copy over confirmation numbers from my checkout screens/emails and paste the next to their corresponding expenses in my digital budget. Takes an extra 3-5 seconds and alleviates some budget anxiety!

…Wanna try this with pen & paper, though? Yeah, I didn’t think so. 😉

4. Sharing is Caring, and It’s Easier Digitally

Need to share your budget with your spouse or loved one? Easy. Just email your digital version over. If you use a budgeting app, many are built to support multiple users for one account.

Your printables require a bit more work to share, however. They can’t be in two places at once. You’d have to snap pics or just wait until you’re both in the same place to look them over and discuss. Not impossible, just not ideal.

5. Day to Day Tracking is a Lot More Likely with Physical Budgets

At least this was the case for me. I went from checking in on my spreadsheet every 5-7 days (gulp) to faithfully devoting 10-15 minutes EVERY DAY to updating expenses and monitoring progress using my worksheets. I find myself actually wanting to interact with the pages. There’s fulfillment in personalizing them with stickers, using my favorite colors to fill in the tracker illustrations, etc. It doesn’t feel like a chore to update my budget these days. It’s colorful and fresh and fun!

6. Cash Envelopes: The GEM of Budget Printables

When I say “physical budget,” I don’t just mean worksheets. I mean all the heavenly paper products that accompany them, too! This includes cash envelopes.

If you notice that printed worksheets liven up your budgeting experience and increase your discipline but you don’t yet use cash envelopes, I’m about to blow. your. mind.

Take a look at our results making the switch to cash envelopes for just ONE category – dining out.

Our 2019 monthly budget for dining out (I’m not even including groceries)…was $800.

O_o

That’s INSANE. (I mentioned bad habits earlier, right?)

I knew once I left active-duty and started making significantly less money, this was going to have to stop. So I put together my first cash envelope and said to myself, ‘Why the heck not?’

I gave us $200 that first pay period. ($400 for the month.) That’s right, I slashed our amount in HALF. I was playing no games.

And you know what happened? We have yet to reach that $200 limit, and we’ve used this method for four consecutive pay periods now.

Cash handling changes your perspective on spending your hard-earned money. Simply put, you’re less likely to do it.

Along the same lines, savings challenges add an element to your budget that can lead to serious savings. For example, March Money Madness proved to be worthwhile, as I saved $85.80 in my personal account for the month by the time the challenge was finished.

7. No More Scanning Pages

I’ve seen peers scan their budgets, page by page at the end of the year, onto external hard drives. It makes me cringe! You’ve gotta remove the binding, insert 20-25 pages at a time into your scanner, make sure it all makes its way to the drive, make sure it’s all in order – what a MESS! There’s an easier way, friends.

Simply save all of your digital budgets on your computer into a budgeting folder. I keep mine right on the desktop. Name them in a way that makes sense and make sure that you have the most recent versions saved. That’s it! Like I said, when you start and end on the digital budget and just use the worksheets for day-to-day upkeep, you really can’t go wrong.

8. Two Peas in a Pod

A digital budget and a printed one and truly an amazing pair. They both represent you and your family’s goals/accomplishments, but they each fill in what the other lacks.

You won’t get the therapeutic results of coloring in a savings tracker or challenge when you are working with your e-budget.

Similarly, you won’t get automatic/integrated calculations and visuals working with pen and paper.

The two need each other to make up a whole financial solution!

Now that I’ve seen the power of this two-part budgeting system, it’s become a go-to recommendation for those seeking a boost financially. By getting you more connected to the details and your day-to-day habits, you open the door to big changes and big results!

So – who’s ready to take this on?!

See you soon!